ETF Tax Traps: CGT, Cost Base Adjustments And Better Records

ETF investing can feel simple. You buy regularly, you reinvest, and you hold for the long term while your distributions appear in your bank account. Then, at tax time, some of the information may even appear in your ATO pre-fill.

Simple, right?

Not always.

Navarre Trousselot, founder of Navexa, recently joined Owen Rask from Rask Media on the Australian Finance Podcast to talk through one of the most overlooked parts of ETF investing in Australia: tax record keeping.

The discussion covered capital gains tax, parcel selection, annual ETF cost base adjustments, proposed CGT changes and why relying on pre-fill alone can give investors a false sense of security.

The simple version of CGT

In simple terms, capital gains tax (CGT) starts with a basic idea: you buy an investment for one price, and if you later sell it for more, you may have a capital gain. If you sell it for less, you may have a capital loss.

But that simple version only gets you so far. Once you have bought the same investment more than once, you no longer have just one purchase to think about. You have multiple parcels.

For example, if you buy an ETF every month for a year, that gives you 12 separate parcels. Each parcel may have a different purchase date, purchase price and cost base. When you later sell only part of that holding, the tax question becomes more complicated:

Which parcels did you sell?

That matters because different parcels can produce different capital gains or losses.

Why parcel selection matters

In Australia, investors can generally choose which parcels are treated as sold, provided their records support the choice. That flexibility can be useful, but it also means the responsibility sits with the investor.

ATO pre-fill may include some investment income data, but it cannot know which parcels you have chosen to sell. That part depends on your own records and the method you apply.

This is where many investors run into trouble. They may assume their broker, ETF provider or the ATO has handled everything. But when it comes to CGT, the parcel-level detail still matters.

A simple example:

You buy the same ETF three times:

- $100 per unit

- $110 per unit

- $90 per unit

Later, you sell some units for $140.

The capital gain may look different depending on whether the sold units are matched to the $100 parcel, the $110 parcel or the $90 parcel.

Same holding. Same sale price. Different tax outcome.

That does not mean one method is automatically right for every investor. It means the records and calculation method need to be clear, consistent and supportable.

The ETF trap many investors miss

The bigger issue comes with ETFs. ETF distributions often feel like dividends. Money appears in your account, and later you receive an annual tax statement from the ETF provider.

That statement may break down the distribution into different tax components, such as franked income, foreign income, capital gains or other categories. Some of those figures may flow into your ATO pre-fill.

But ETFs can also create cost base adjustments.

These adjustments may increase or decrease the cost base of your ETF holding. That can affect your future capital gains calculation when you eventually sell.

The key point is simple: your ETF tax statement may not only matter for this year’s income. It may also affect the future CGT calculation for the parcels you continue to hold.

Why cost base adjustments can compound over time

This is the part many long-term ETF investors miss.

Say you invest into an ETF every month for 10 years. That could be 120 separate parcels.

If your ETF annual tax statement includes a cost base adjustment, that adjustment may need to be applied across the relevant parcels. Then the next year’s statement may affect the parcels you already held, plus the new parcels you bought during that year.

Over time, this can create a cascading record-keeping problem.

It is not just:

- What did I buy this year?

- What parcels did I hold?

- What cost base adjustments applied?

- In what order did they apply?

- What did I sell in previous financial years?

- Which parcels are still available?

When you eventually sell, your CGT calculation may rely on years of historical data.

Why this may become more important after proposed CGT changes

The 2026 Federal Budget included proposed changes to capital gains tax rules. Based on current public reporting, the proposed changes may replace the 50% CGT discount with a cost-base indexation model for certain assets from 1 July 2027. There has also been discussion of a minimum 30% tax rate on net capital gains.

These changes should not be treated as final until the legislation and guidance are clear. The details may change. Different assets, entities and investor circumstances may be affected differently.

But the practical takeaway is clear: better records may become even more important if the proposals proceed.

If an investor owns assets before 1 July 2027 and sells after that date, the calculation may require more than one tax treatment across the life of the investment. That could make historical parcel records, cost base adjustments and valuation data more important.

For ETF investors, that is where things may become particularly messy.

If you have not been tracking ETF cost base adjustments properly, future CGT reporting could become harder to reconstruct.

Pre-fill is useful, but it is not a full tax record

ATO pre-fill can be helpful. But it is not the same as a complete portfolio tax record.

It may help with some income fields. It may include data provided by institutions. It may reduce manual entry.

But it does not remove the need to understand:

- which parcels you bought

- which parcels you sold

- which parcel selection method you used

- whether cost base adjustments applied

- what happened in previous financial years

- which records your accountant may need

That is especially important if you dollar-cost average, reinvest distributions, use DRP, own ETFs, sell partial holdings or change your CGT method between years.

The mistake of treating tax as a one-year problem

A common investor mistake is treating each tax year in isolation.

They might sign up to a tool in June or July, generate a tax report for the year, then stop tracking once the return is lodged.

The problem is that investment tax does not always work neatly one year at a time. A parcel sold this year may have been bought five years ago. An ETF cost base adjustment from three years ago may still matter. A sell trade from a previous year may determine which parcels are still available now.

This is why tax reporting is not just about generating one report at tax time.

It is about maintaining the records that make the next report easier, cleaner and more defensible.

Why screenshots and AI prompts are not enough

AI can be useful. It can explain concepts, summarise data and help investors ask better questions.

But a screenshot of your brokerage account is not enough to calculate your tax correctly.

A screenshot may show that you own 100 units of an ETF. It may show the current value. It may even show the average price.

But it usually will not show every parcel, every historical buy, every sell, every DRP entry, every cost base adjustment and every method used in previous financial years.

Without that data, any CGT calculation is incomplete.

That is why the underlying records still matter.

AI can help make portfolio data easier to work with. But for tax reporting, the maths needs to be based on accurate, complete data and consistent calculation logic.

How Navexa helps investors stay organised

Navexa is built to help Australian investors track portfolio performance, income, realised gains, unrealised gains and tax reporting in one place.

For investors dealing with CGT, ETFs and long-term records, Navexa can help by keeping portfolio data structured across financial years.

That can make it easier to:

- track holdings and parcels

- review realised capital gains and losses

- understand income and distributions

- record ETF tax statement data

- compare supported CGT allocation methods

- keep a clearer record for tax time

- prepare information for an accountant or tax adviser

Navexa does not provide personal tax, financial or legal advice. But it can help investors organise the data they need to have better conversations with qualified professionals.

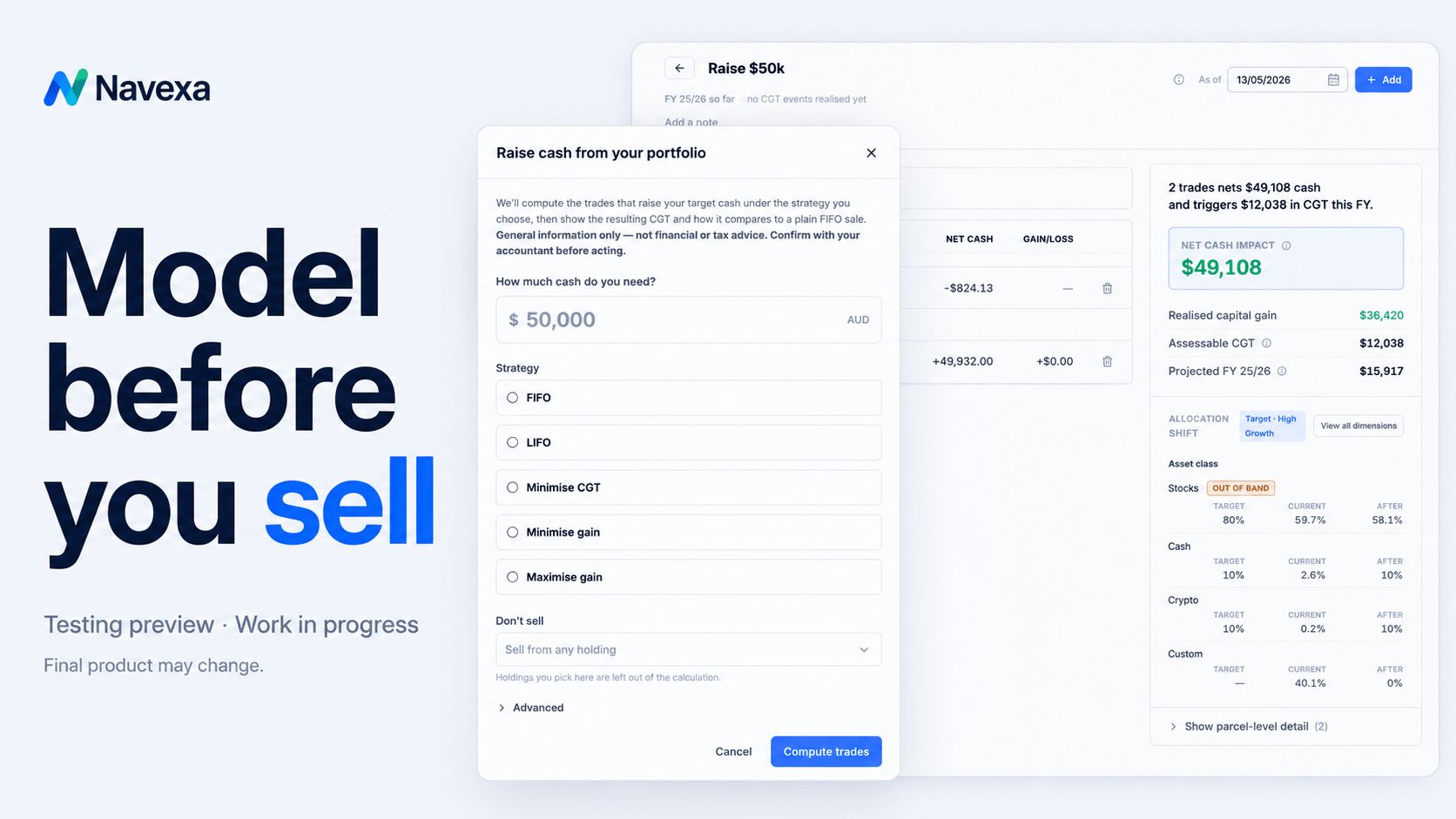

Tax-aware rebalancing and trade simulation

During the webinar, Navarre also previewed development work around trade simulation and tax-aware rebalancing.

The idea is simple. Before selling, investors often want to understand what the tax impact may look like.

For example:

- What happens if I sell this holding?

- What if I need to raise $10,000?

- What if I rebalance back to my target allocation?

- What is the estimated realised gain or loss before I place the trade?

This type of workflow can help investors see the tax side of a potential transaction before they act.

It is not about telling investors what to buy or sell. It is about showing the maths based on the portfolio data, chosen settings and available records.

That distinction matters.

Good software should not replace professional advice. But it can give investors better visibility before they make decisions or speak with their accountant or adviser.

A practical ETF record-keeping checklist

If you invest in ETFs, here are some general records worth keeping organised:

- Broker contract notes for buys and sells

- Dividend reinvestment plan records

- ETF annual tax statements

- AMIT or AMMA statement details where relevant

- Cost base adjustment information

- Distribution income details

- Previous year CGT reports

- Notes on which parcel method was used

- Records of any manual parcel selection

- Accountant adjustments or tax return decisions

The more often you invest, the more important this may become.

Monthly investing, DRP, multiple ETFs and partial sales can all increase the number of records involved.

The main takeaway

ETF investing may be simple from an investment strategy point of view.

But ETF tax reporting can be much more complex than many investors realise.

Pre-fill can help. Broker data can help. Annual ETF tax statements can help.

But none of those things automatically remove the need for accurate, parcel-level records.

If proposed CGT changes proceed from 1 July 2027, that record-keeping burden may become even more important.

Better records. Better visibility. Better reporting.

That is the practical lesson from Navarre’s discussion with Owen Rask.

Frequently Asked Questions

Are ETF distributions the same as dividends?

Not exactly. ETF distributions may include different tax components, depending on what happened inside the fund. Your annual ETF tax statement may break these components down for tax reporting.

What is a cost base adjustment?

A cost base adjustment changes the cost base of your holding. In simple terms, it can affect the capital gain or loss calculation when you later sell the investment.

Does ATO pre-fill handle ETF tax completely?

Not always. Pre-fill may include some income information, but investors still need to consider CGT, parcel selection, cost base adjustments and their own records.

Why does parcel selection matter?

If you bought the same holding multiple times, each parcel may have a different price and date. When you sell part of the holding, the parcels selected can affect the capital gain or loss calculation.

Will the proposed CGT changes definitely happen?

The rules discussed are proposed and subject to final legislation and guidance. Investors should follow official updates and speak with a qualified tax professional about their circumstances.

Does Navexa give tax advice?

No. Navexa provides portfolio tracking and reporting tools. It does not provide personal financial, legal or tax advice.

Start tracking your portfolio with more clarity

Navexa helps Australian investors track performance, income, realised gains, unrealised gains and tax reporting in one platform.

If you invest in shares, ETFs, crypto or other assets, clearer records can make a big difference at tax time.

Explore Navexa to see how better portfolio tracking can help you stay organised.

Disclaimer: This article is general information only and does not constitute financial, legal or tax advice. It does not take into account your personal circumstances. The tax changes discussed may be proposed, draft or subject to final legislation and guidance. Details may change. Navexa provides portfolio tracking and reporting tools, but does not provide personal advice. Always speak with a qualified tax professional, accountant or financial adviser before making financial, legal or tax decisions.